solution

solution.

a. Janet Meer is a fixed-income portfolio manager. Noting that the current shape of the yield curve is flat, she considers the purchase of a newly issued, option-free corporate bond priced at par; the bond is described in Table 11.9 . Calculate the duration of the bond.

Save your time - order a paper!

Get your paper written from scratch within the tight deadline. Our service is a reliable solution to all your troubles. Place an order on any task and we will take care of it. You won’t have to worry about the quality and deadlines

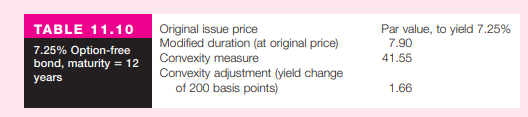

Order Paper Nowb. Meer is also considering the purchase of a second newly issued, option-free corporate bond, which is described in Table 11.10 . She wants to evaluate this second bond’s price sensitivity to an instantaneous, downward parallel shift in the yield curve of 200 basis points. Estimate the total percentage price change for the bond if the yield curve experiences an instantaneous, downward parallel shift of 200 basis points.

"Looking for a Similar Assignment? Get Expert Help at an Amazing Discount!"